How can steward-ownership be legally implemented?

Legal structures for implementing Steward-Ownership

Summary

There are four basic models of implementing steward-ownership worldwide: foundation models, trust models, veto-share models and own legal forms for steward-ownership.

Steward-ownership can be implemented using different legal forms depending on the type of company and jurisdiction. All of the ways of implementation have in common that they enshrine the two principles of steward-ownership and secure them legally in the long run:

1. Self-governance

The voting rights, or "steering wheel," of the company remains inside the company with the people directly connected to stewarding its operation and mission. They assume the entrepreneurial responsibility for the actions, values, and legacy of the company as stewards for the company and for future generations of stakeholders.

2. Purpose-orientation:

The company's assets cannot be privatized by shareholders but remain tied to the company. The company's profits and assets are thus a means of working towards the company's purpose and not purely an end in themselves. Profits are reinvested, used to cover capital costs or donated.

This is often realized through a separation of the voting rights and the economic rights of the company: the property rights of the company are not treated as one bundle of rights anymore, but are distributed separately to uphold the principles of self-determination and purpose-orientation. The implementation of steward-ownership is often realized through a combination and/ or modification of different legal forms to achieve the desired outcome.

Why make it legally binding?

You might ask why to enshrine the principles in law at all. They could be agreed on and followed within a company even without legal anchoring – as many companies actually already do. The entrepreneurs do not see themselves as asset owners of the company but as stewards. So what is changed through a legally secure implementation?

Coherence of corporate culture and legal structure

For many entrepreneurs, the main reason for legally implementing the principles of steward-ownership is that they are seeking for more coherency between the lived corporate culture and the legal structure. To many, it does not feel coherent to own the company as an asset (and to be able to realize its value by selling it) whilst thinking and communicating that the company exists to serve its purpose.

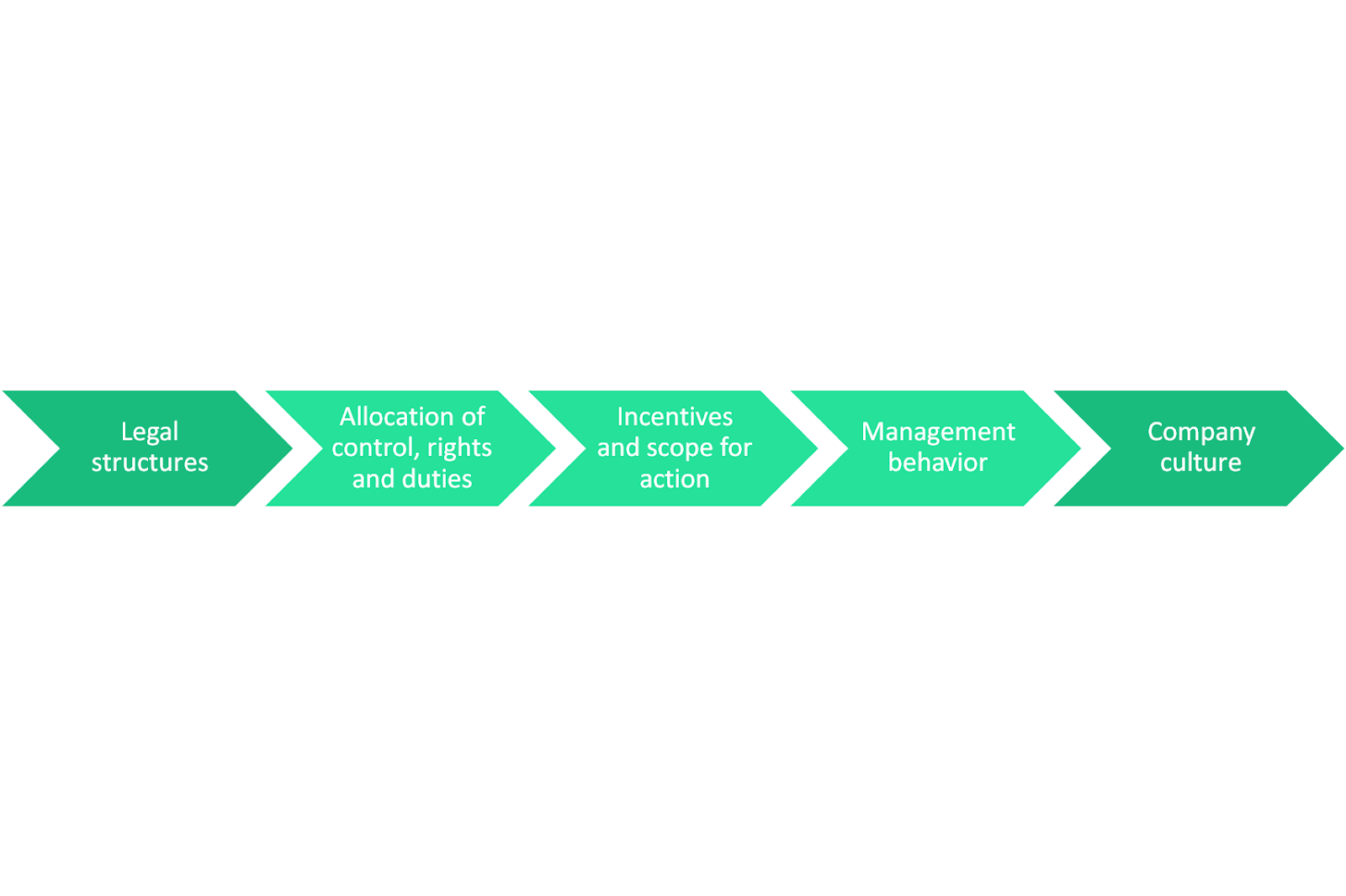

This is linked to the argument that the legal structure of a company has a direct impact on its corporate culture in the medium to long term. The legal structure largely determines the distribution of rights and obligations between the parties involved and determines who has control over the company. The legal framework thus determines the scope of action of the decision-makers and sets incentives for decisions and actions. These incentives have a directing effect on the management and thus shape the corporate culture in practice.

Another important factor is that the intergenerational security of steward-ownership depends on the legal structure. While you can live the principles without reflecting them on a legal level, their upholding will always be dependent on the individuals holding the ownership rights of the company. If the principles of steward ownership are anchored in the ownership structure in a legally binding way, they will also apply to future generations of entrepreneurs – this cannot be guaranteed in the long term without legal implementation.

Of course, another argument for legal implementation is the communication of steward-ownership: If an entrepreneur wants to make a binding promise to all stakeholders today that the values of self-determination and asset ownership are secured and binding beyond the spoken word, then the DNA, the ownership structure, must be adapted for this.

Different legal structures for the implementation of steward-ownership

Steward-owned companies enshrine the principles of steward-ownership by using different forms of legal safeguards to ensure them in the long run. There are different models of legally implementing steward-ownership which differ depending on which country you are in, the size and type of the company, the needs of the shareholders with regard to the distribution of profit and voting rights, the involvement of stakeholders and the desired flexibility.

Most companies implementing steward-ownership use a legal operating entity that is owned in a specific form by a foundation or trust. The legal form of the operating entity (the company) in steward-ownership varies; examples include limited liability companies or corporations as well as cooperatives.

Foundation & Trust Models

If the legal system you are operating in allows trusts or foundations – self-governing entities without shareholders that allow for a long-term focus on a specific purpose – chance is that foundation-/trust-ownership is an option to implement steward-ownership. However, foundation and trust law vastly differ between different legal systems, so even if they exist in a specific legal system, it is not a given that they can be used for entrepreneurial purposes.

Single Foundation

The shares with voting rights and dividend rights of a company are held by a self-governing non-profit institution (foundation) that acts as shareholder and guardian of the steward-ownership structure and principles. The primary purpose of the foundation is to own the company shares and further the purpose and development of the company. The foundation can additionally follow further non-profit purposes.

Single-foundation institutions often have two boards: one that holds the controlling rights of the company, and one that holds the rights to distribute dividends to charitable causes. The separation of boards ensures there is no conflict of interest between the charitable and operational arms of a business.

While this model is prevalent in Denmark, it is less common in other countries because of legal regulations in foundation law. Single-foundation models are also widely used in the Netherlands, in part because they can also be set up as so-called “STAK” companies – a sub-form of foundations that are allowed to issue economic certificates. In a STAK, a foundation controls the company, but can grant shares that carry economic rights with limited or no voting rights.

Zeiss (Germany), Novo Nordisk (Denmark) and Carlsberg (Denmark)

Double Foundation

The set-up of a Double Foundation model necessitates three legal entities: the operational entity (the company) and two foundations or other legal holding entities. The model separates voting rights and dividend rights of the operational entity completely by placing them into two separate legal entities:

- Dividend rights are held by a charitable entity (often a foundation), while voting rights are kept in a trust or foundation that is managed by stewards. Stewards can be the current leaders of the company, a combination of current leaders, previous leaders, and external independent supervisors (as in the case of Bosch), or exclusively external independent and former leaders (like Mahle or Elobau).

- The voting rights (but no dividend rights) of the company are held by a stewarding organization managed by stewards of the company. A charitable entity holds the dividend rights and the majority of capital shares of the company, but no voting rights.

Thus the separation of power and money is reflected on the legal level. Because of this clear separation of voting and economic rights, the trust foundation model is particularly effective for decoupling profits from charitable contributions. There is no mechanism in this model for the charitable arm to pressure the company to generate more profits for its charitable purposes.

Perpetual Purpose Trust

The Perpetual Purpose Trust (PPT) is a trust that is established for the benefit of a purpose rather than a person. Unlike most trusts, which have a limited life-span, a PPT may operate indefinitely. PPT’s are governed according to a purpose set forth in a Trust Agreement, a document which redefines the legal fiduciary duty of its trustees (trust stewardship committee). For the implementation of steward-ownership, the shares of the operating entity (the company) are held by the PPT. The trustees control the PPT, but do not have access to the value or profits of the company.

Organically Grown Company, as well as the Breaking Ground Perpetual Purpose Trust in the US.

Employee Ownership Trust

A specific set-up of employee ownership trust models can be used to implement steward-ownership. The shares of the operating entity are held by an employee ownership trust, which is indirectly controlled by the employees of the company. The speciality of employee ownership trusts with steward-ownership is that the employees can only participate in the success of the company in a very limited way (see principle of purpose-orientation).

Trust Partnership

In a trust-partnership, a company is owned by a trust on behalf of a group of partners, most commonly the company’s employees. This structure often blends employee democracy with meritocracy. All partners, or a representative group of partners, participate in the operation of the business and share in its profits. Because each partner only receives a small portion of the profits, e.g., a 13-14th of their base salary, the model still prioritizes purpose over profit, and cannot be compared to normal shareholder-owned businesses in which absentee owners collect all the profits. In many cases, for example in the case of John Lewis, the majority voting right owner is a worker-independent trust that appoints the CEO through a meritocratic process, while workers have the right to fire the CEO.

John Lewis Partnership (UK).

Other models

Golden Share/ Veto Share

In the ‘Golden Share Model’, the principles of steward-ownership are written into the articles of association of the company. Stewards of the company hold 99% of the voting rights, but no dividend rights. 1% of the voting rights classified as a ‘veto-share’ or ‘golden-share’ is held by an independent controlling entity to safeguard the principles of steward-ownership. It has the right and obligation to veto any changes or actions concerning the principles of steward-ownership. No one in- and outside the company has a right to its economic value. Dividend rights either remain in the company or lie with investors and/ or founders. Those rights do not grant unlimited access to dividends but always have to be coupled with a mechanism limiting the right to receive profits.

To implement the golden-share model, a golden-share holding entity is necessary as a controlling shareholder. An organization like this is not available in every region.

Own legal form

In very few countries, there is an own legal form for implementing steward-ownership. Today, this is still not common – and they do not always make a 100% implementation of the principles of steward-ownership possible. One example of an own legal form for steward-ownership is the Community Interest Company in the UK.

There are several countries in which an own legal form for steward-ownership is currently on the way or at least requested by entrepreneurs.

Published by: Purpose Schweiz

Graphics and illustrations: Purpose Stiftung